The setting sun

While rising Japanese bond yields might have made the headlines of late, the real danger lies elsewhere: those countries reliant on foreign savings to finance their chronic trade and budget deficits.

Although not normally a front-page financial topic in Europe or North America, the recent spike in Japanese government bond (JGB) yields did manage to make it to page three or so. There’s talk of Japan being in a “debt-trap”, of a potential future default, and of the financial chaos this might unleash.

While Japan’s debt is indeed a potential problem, in my opinion its significance is way overblown. As with all large economies, Japan has issues. But these are like storms in teacups compared to the challenges faced by the US, UK and euro-area.

Japan is an immensely wealthy country with an equally immense demographic problem. A substantial portion of their highly-productive middle-class is now retired or retiring. They naturally expect a modestly lower income in future as a result. But the Japanese middle-class is also legendary for its high savings rate, well above those in most other “wealthy” countries. After all, retiring is only a potential problem if you haven’t saved for it, no?

Wait a minute, some might interject, doesn’t Japan have a massive government debt? Well yes, as a matter of fact it does. Beginning in the early 1990s, following the collapse of a colossal housing and stock market bubble, Japan began to run large government deficits. It has remained in deficit ever since. The gross government debt/GDP ratio has thus risen relentlessly and stands at some 234% today. Ouch! (Net debt/GDP, incidentally, is much lower, at about 134%. More on that below.)

How rapidly is this debt growing? Well, according to the IMF, Japan ran a deficit of about 2.8% of GDP in 2024. So, the debt pile continues to grow, albeit by a rate only about half that of the US, UK and euro-area economies.

Yes, as it stands now, Japan’s government debt/GDP ratio is higher than the US, UK and most of the euro-area. But let’s put this in perspective: First of all, who owns this debt? Well guess what, the Japanese do. That’s right, their government debt is held almost entirely domestically. They basically owe their debt to themselves.

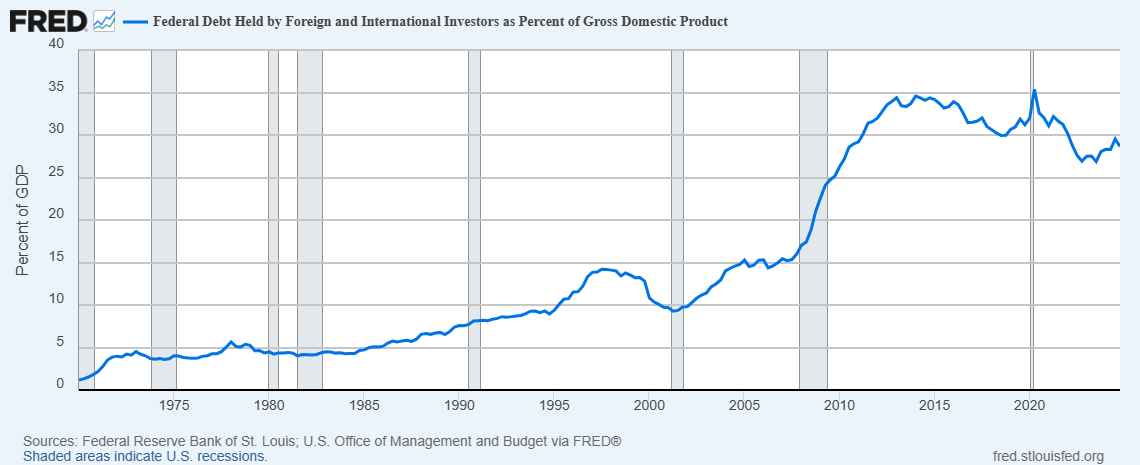

Now, that doesn’t mean that this debt isn’t an issue, but it’s not the same sort of issue as if your government debt is held largely by foreigners, who might decide to sell that debt someday to buy some other country’s debt or to finance domestic investment or consumption. This is a potential risk with the US and UK, which rely heavily on foreigners to finance a substantial portion of their government debt.

Having discussed government finances, this brings us to the most important point of all, which is to compare the entire Japanese economy, public and private, to those of the West. As a legacy of decades of large trade and current-account surpluses with the rest of the world, Japan today has the world’s largest net foreign credit position of some $3tn, whereas the US and UK have large net foreign debt positions, with the euro-area roughly in balance. (1)

US net foreign debt through the decades

Now, why is the net foreign debt or credit position so important? Think about it: If you are approaching retirement, do you want to owe other people money, or do you want them to owe you? Japan may be an ageing society, but it is an ageing society with a private sector that has saved prudently for retirement. Japan may have a huge government debt but it can service that debt for an extended period by gradually winding down its massive net foreign credit position.

Take care what you wish for

But wait, what does this imply? If Japan is now beginning to gradually “dis-save” in this manner, gradually selling off its large accumulated holdings of US Treasuries and other foreign assets to service its domestic debts, what is going to happen to interest rates and currencies? Well, if Japan is winding down its holdings of US Treasuries and exchanging the proceeds for yen cash to service Japanese government debt then, other factors equal, US Treasury yields are going to rise and the dollar fall versus the yen.

Rising yields will crimp US growth and a weaker dollar will reduce US purchasing power, such that demand for Japanese exports will likely decline. But then, if Japan is indeed dis-saving, it will be less reliant on exports anyway, especially to the US, which in any case has been declining in importance for Japan for years as its Asian neighbours have been growing faster as a source of demand.

Viewed in this way, Japan’s demographic issues, far from being automatically yen negative, could in fact be yen positive, at least for some period of time. Yes, Japan’s potential growth rate may be in gradual decline for demographic reasons, but at least they have a huge stock of private savings. And as they wind down their holdings of foreign assets, stocks and bonds, and exchange the proceeds for yen, the value of those assets will come under downward pressure, as will their currencies of issue versus the yen.

One objection that might be raised at this point is that perhaps, notwithstanding a large net foreign credit position, Japan’s private sector has nevertheless not saved enough to fully fund its demographic-driven future liabilities. Fair enough, in fact I would agree that it hasn’t. But who has? Please name one large developed country that has fully-funded future liabilities, public and private.

Can’t do it? Well that’s because there isn’t one. (There are some smaller ones, including Norway for example.) The US, with estimated future public liabilities of some six times GDP may be the most egregious example of massive, largely unreported off-balance sheet obligations such as Medicare, Social Security, etc, but it is nevertheless in good company with the UK and several euro-area countries.

Moreover, whereas Japanese corporations and also the public sector tend to have essentially fully-funded pension plans—the primary explanation for why Japan’s net public debt is so much lower than gross public debt—the same cannot be said for most US, UK or European corporations and public sector entities, many of which are already facing pension funding problems, requiring additional debt issuance just to make interest payments.

Now, how on earth is that new debt going to be serviced? I’d much rather be in line to receive a fully-funded Japanese pension—despite the ugly demographics—than a ponzi-style pay-as-you-go and hope-the-stock-and-property-markets-always-rise, western-style one.

Another point that is worth mentioning here is that the normal Japanese retirement age is only 60, yet the Japanese are generally much healthier and longer-lived than their western counterparts, and also tend to have a stronger work ethic, implying that it could be quite possible to increase the retirement age substantially, thereby generating additional income and holding down retirement costs.

That could have a huge impact on their ability to deal with their demographic problem, at least for a number of years. Several western countries have large and growing chronic health issues which suggest that, even if retirement ages are extended somewhat, they may not be able to reap the same degree of productivity benefits as comparatively healthy Japan.

Finally, much ridicule has been directed at Japan’s relentless and ultimately futile attempts at fiscal stimulus over the past few decades. But consider: Rather than transfer cash to households to spend on food, or vacations, or whatever, stimulus in Japan has generally taken the form of investment in infrastructure, such as “bridges to nowhere”, for example.

Even “bridges to nowhere” aren’t completely worthless

Now, I’m no fan of misguided Keynesian stimulus, which at the extreme is as counterproductive as paying people to dig holes and then fill them up again, but if I had to choose, I’d probably choose to own a bridge to nowhere or other such infrastructure rather than an empty hole in the ground. The former might at least be of some value, if less than what a profit-seeking corporation would have built with the capital instead.

If Japan does get into budget difficulties down the road that cannot be fully addressed by increasing the retirement age; raising taxes; restructuring pension liabilities; drawing down net foreign savings, etc, then Japan has much public infrastructure which could be privatised to raise funds. After all, this has been going on in western economies for years. So much public infrastructure has already been sold off in some places that there is not much left.

In the US, even state capitol buildings have been sold (and leased back) to raise revenue for cash-strapped governments. Japan has not even begun to go down this road, which given the huge numbers of “bridges to nowhere”, might be long indeed. The West, however, has mostly reached the end, leaving it with fewer options.

We know what happens to countries that have borrowed too much and can’t pay it back. They devalue their currencies, default on their obligations, or both. However, if you owe the debt largely to foreign, rather than domestic investors, isn’t it politically more expedient to devalue, than to default? As a result, might the political temptation to devalue unfunded liabilities away be much greater in the US or UK than in Japan?

I believe so. And I’m hardly alone. Much of the rhetoric coming from Trump’s economic team echoes this sentiment. There is a growing willingness to discuss the US’s unsustainable public debt situation, including an extreme reliance on foreign savings to plug the gaps. Tariffs and dollar devaluation are no longer taboo subjects.

Perhaps someday there is going to be some sort of restructuring of Japanese government debt, but as they owe it primarily to themselves and are only now just beginning the long process of dis-saving, implying less reliance on exports, I don’t see nearly as much potential risk of a pro-active devaluation of the yen as I do for the dollar or sterling, where savings rates and exports, in fact, need to rise dramatically to rebalance those economies.

Now, with Trump in the White House following a populist surge, it is not just the economics of foreign asset sales that favour the yen over the dollar but, at the margin, also the politics. Take care what you wish for, America.

(1) It is an economic identity that, if you export more than you import, you run a trade surplus which, when broadened to include all cross-border transactions, including interest payments for example, is called a current-account surplus. Over long periods of time, cumulative current-account surpluses, or deficits, can become large and, in the past, have occasionally been associated with major international financial crises. This is one reason why many observers have been concerned in recent years with the growth of global imbalances, in particular that of the US, which has been running large deficits, and China, which has been running large surpluses. In key respects, the current set of global imbalances is eerily reminiscent of the 1920s, when the US was running large surpluses and the UK large deficits, a legacy of massive WWI spending and economic upheaval. While economic historians disagree on the specifics, there is general agreement that the large and growing global imbalances in the 1920s contributed to the severity of the Great Depression that began during the global financial crisis of 1929-33.