Carried away

Prices are set at the margin. This includes the price of US assets which are, at the margin, held by foreign investors. A US funding crisis may be closer than you think.

Yesterday I wrote about the recent spike in Japanese government bond (JGB) yields and why this isn’t necessarily a problem for Japan. It is, however, a potential problem for the US, as the Japanese hold a huge portion of US debt.

When investors purchase holdings of foreign assets they have a choice of how to finance their holdings. They can do so in domestic currency—thereby directly taking the foreign exchange risk in the position—or they can finance in the currency of the foreign asset itself eg fund dollar assets with dollar borrowings.

While both are common in practice, when it comes to Japanese holdings of US assets specifically, a huge portion of these positions are financed in yen. Japan’s total net foreign credit position is a colossal $3tn, with US assets being the majority part.

For decades, global financial markets have been driven in part by so-called carry trades, or convergence trades. Both share the common characteristic of sourcing cheap funding, wherever to be found, in order to purchase a higher yielding asset. Borrowing in yen to fund dollar asset positions is a classic example.

It’s a form of arbitrage, albeit one not without risks. A sudden reversal in European convergence trades in 1998 led to the failure of prominent hedge-fund Long-Term Capital Management. In August 2024, a surprise rate hike by the Bank of Japan (BoJ) triggered the so-called “mini crash” that saw many US tech stocks drop by double-digits in a single day.

Carry trade transmission

How, exactly, does a BoJ rate hike trigger a US stock market crash?

Well, if yen interest rates lie below those of other major countries, then traders seeking cheap funding will borrow in yen to fund positions in higher-yielding assets elsewhere. These could include those where the expected returns are high, such as US “Big Tech”.

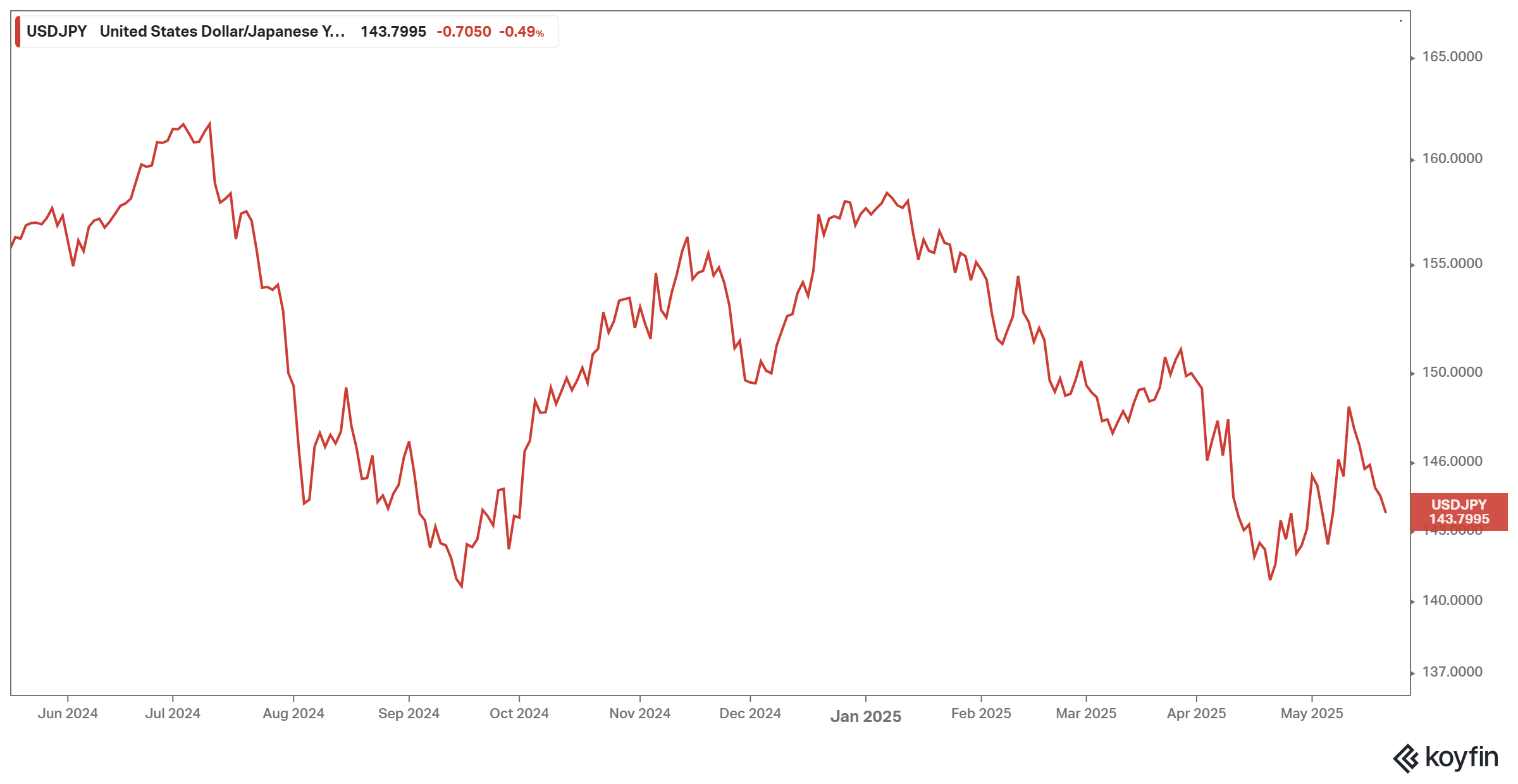

This was the case going into the flash crash. The BoJ raised rates and the yen spiked higher, strengthening from over 160 per US dollar to nearly 140 in just a matter of days. That caused big losses for those traders short the yen. Some were forced to liquidate positions as a result of margin calls. They got carried away, as it were, if not on stretchers.

A few months later, Trump was elected president and the markets recovered. Attention turned elsewhere. Then tariff and trade war risks entered the headlines and stocks stumbled again.

But notice what you see in the chart above: the yen has been strengthening again in recent days as JGB yields have risen, possibly due to fears of another BoJ rate hike.

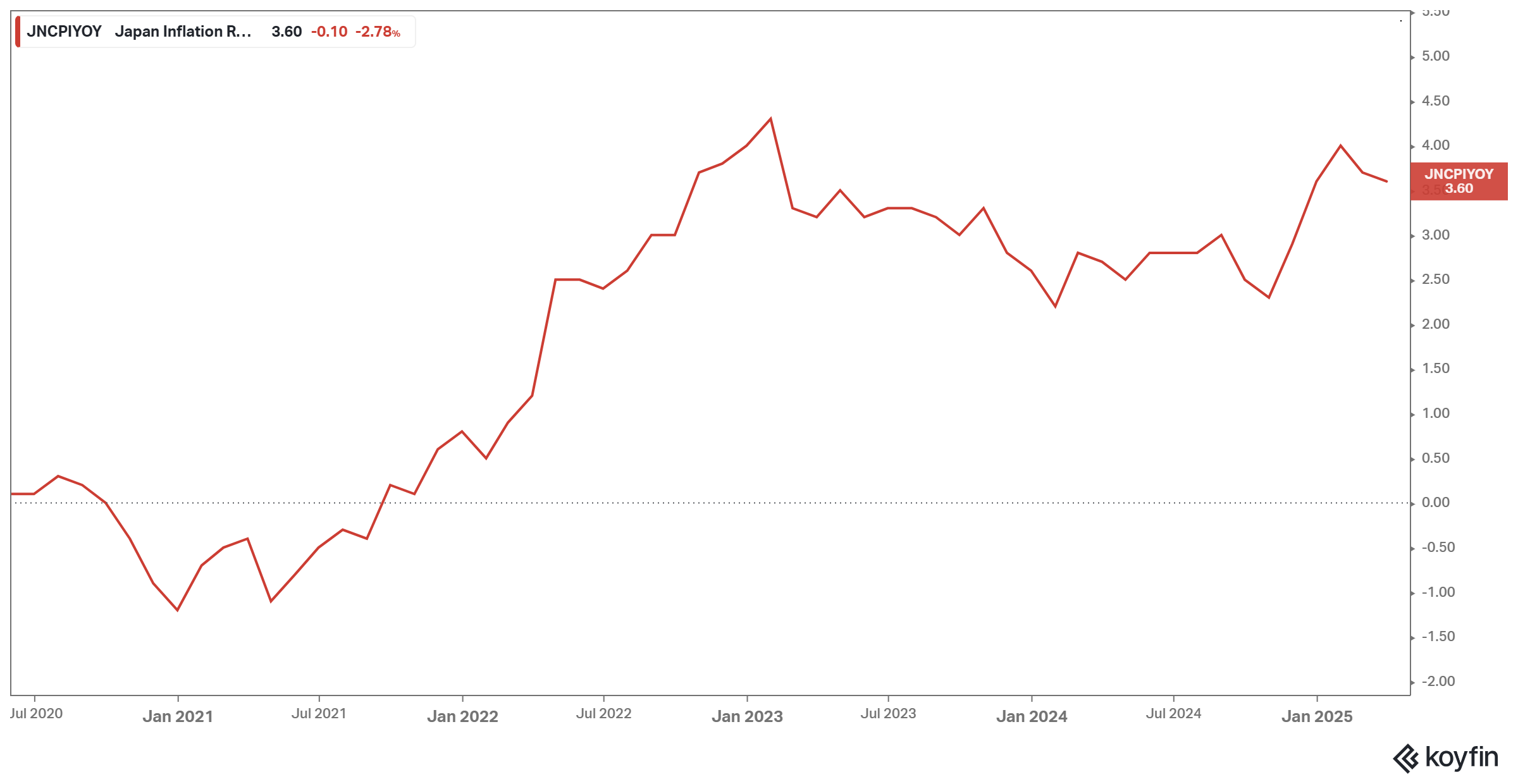

Why would the BoJ hike rates? The global economy is weak and perhaps sliding into outright recession.

But in Japan, inflation has been rising again and is now close to its highest level for many years. (There was a brief spike in 2023 that was a temporary base effect related to the ending of global Covid lockdowns.)

There is thus good reason for JGB yields to be higher and for the yen to be stronger.

And good reason for carry traders to be nervous.

If the BoJ raises rates further, JGB yields keep rising and/or the yen continues strengthening, something along the lines of August 2024 could unfold again. It might not be as sudden and dramatic but it would weigh on markets nonetheless.

Could a renewed rush to reverse carry trades stop the recent stock market recovery in its tracks? Absolutely. Add it to the list of risks.

More reasons for caution

The fact is, at present there are many reasons for caution. It doesn’t help matters that President Trump is pushing hard to get his “big, beautiful” budget bill through the Congress, one that would practically guarantee at least a few more years of unusually large US budget deficits and, by implication, unusually large US Treasury issuance.

That could place upward pressure on US rates and credit spreads, with negative implications for US finances generally. If combined with a yen carry trade unwind, the spike in US borrowing costs could be all the greater.

Tariff and trade war concerns remain elevated, and their potential impact is nearly impossible to predict. With today’s intricate global supply chains and value-added networks, even experts struggle to model the full extent of the damage. Multinational corporations probably can’t even precisely model the impact on their own businesses.

Global stock market valuations remain historically elevated, especially in the US. But that’s due largely to the extremely high multiples placed on a small number of companies, including the Magnificent Seven tech firms.

Never in history have such a small number of firms so dominated global stock markets, especially those reliant primarily on “intangibles”, such as brand value or intellectual property, for their lofty valuations.

There is a saying that bull markets always climb a wall of worry. I agree. But once you’ve climbed that wall to historically high valuation multiples, seemingly small things can have a disproportionate impact on prices.

Merely a return to a modest, sub-20 price-to-earnings (P/E) ratio for the S&P 500 would send prices down by about 1/3. Again, most of that might be due to a sharp correction in the Big Tech sector. But it is hard to imagine the broader market escaping with less than a double-digit percentage decline.

It could be far worse than that. I’ve written before how rising tariff and trade war fears were likely the proximate cause for the October 1929 US stock market crash, one that would eventually wipe out some 90% of market value.

That’s not a prediction, merely an observation. But were the market to crash this year, it would be yet another example of history not exactly repeating, but certainly rhyming.